Don’t miss our analyst key picks for the year ahead and allow for your questions to be answered live – register today to attend Stock Doctor’s Reporting Season Recap Live Webinar.

In the lead up to the December half 2023 reporting season, analysts were revising down their expectations for corporate earnings due to the flow on impact of rising rates and slowing business confidence. Cyclical sectors such as consumer discretionary, building materials and resource stocks were feeling the brunt of it, as their earnings are most leveraged to the economic cycle, and institutional investors did not want to be exposed to stocks at risk of a downgrade.

Fast forward 4 weeks and the ASX earnings results were perhaps not as bad as originally feared. Hooray! Markets are now soaring to new highs, and every signal in the book is telling you that the risk on rally is back in full force (I’m looking at you Bitcoin). To be frank, we’re not convinced.

Slow Your Roll

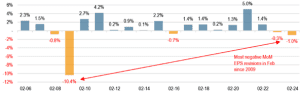

According to bottom-up market data from JPMorgan, earnings revisions across February have been the weakest since February 2009. This came down to softening margins, rising interest expenses and greater expenditure planned for the year ahead.

Source: Bloomberg, JPMorgan

These are aggregate figures, and a lot of this data can be explained by the heavy revisions within the resource sector. Lower commodity prices, asset impairments and rising costs have resulted in a net earnings decrease of circa 25% for FY24 within resources, which is dragging the ASX data down given its large weighting. Still, this is an ugly datapoint for those who are reporting that this was an excellent reporting season for the ASX

Share Prices Up, Earnings Down

As mentioned in the opening paragraph, consumer discretionary was one of the sectors experiencing negative earnings revisions heading into reporting season, and the sector was heavily sold off prior to the new year.

Source: Stock Doctor

According to our data on Stock Doctor – 5 companies within the sector are showing positive earnings revisions of over 10% post reporting season (representing large beats). Notably, of the 5 companies (ASX:KGN, ASX:CTT, ASX:TPW, ASX:NCK, ASX:JBH), 2 are forecast to have their earnings fall by ~20% (NCK, JBH) for the full year and yet the minimum total shareholder return over 1 year is approaching 50%! The results are clear. The market is brushing aside near-term earnings weakness overall and responding to the hopes of rate cuts, a soft-landing scenario and a return to explosive earnings growth in FY25.

Even if we assume these economic forecasts play out, company share prices are already reflecting this perfect outcome in their market valuations. Hence in our view,the risk to reward ratio in this sector is starting to look puzzling. And what would happen if the economic landscape were to change? In such a scenario there is major downside to prices.

Multiple Driven Market

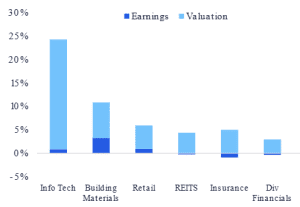

We’ve showcased data that tells us earnings revisions were poor for reporting season, despite large share price reactions to the upside. We’ve highlighted that even companies with EPS decline of 20% are “outperforming” the market. And below, we highlight that the total market earnings for FY24 are anticipated to be poor overall.

Source: Macquarie Research

So, what is driving our market higher? The answer in the short term is P/E multiple expansion. Data generated by Visible Alpha and collated by Citi Group eloquently displays the sheer level of multiple expansion within some of the most discussed sectors of reporting season.

Source: VA, Citi

Another driver of multiple expansion is the amount of capital flowing into passive ETF vehicles as investors increase their overall asset allocation to equities. We discussed the secondary impacts on markets that staggering passive ETF flows cause in a previous article: Read Here (which we encourage all investors to read).

Stock Doctor members should be familiar with the stellar performance of the tech sector through our Star Stocks Wisetec (ASX:WTC), Altium (ASX:ALU) and RPM Global (ASX:RUL) which all rose more than 30% during the month. Whilst this is a nice feeling to experience for our and member’s portfolios, we are acknowledging that this level of price appreciation appears overdone and if anything, represents an opportunity to take some profits off the table in the near term. Yes, they are fantastic businesses with excellent fundamentals, but we must be realistic about what the market wants to price into the stock in the near term. It is simply appearing too optimistic across the board.

Source: Stock Doctor

So How Should Investors React?

Our members are well aware that our managed fund’s are utilizing ETFs to hedge our exposure to the overall market in the near term. The introduction of levered inverse market ETFs, such as BBOZ, allows the fund team to effectively reduce volatility for unitholders. While this means we won’t experience the full extent of explosive gains to the upside, we will mitigate the vast majority of risk to the downside. One may view this as too conservative an approach – but our view is that we are being prudent in times of uncertainty and greed. The below chart depicts the extent of extreme investor sentiment in the marketplace at the moment.

Source: CNN Fear and Greed Index Oscillator

You can see here that the momentum in the market is being carried by greed, and if history is a guide, sentiment can shift very quickly when hope is so high.

Opportunities in Today’s Market

We are building out our knowledge and understanding of companies that we believe had fantastic results, and would like to add to our portfolios, but are sitting on the sidelines until the risk/reward ratio appears in our favour. Some examples of companies in our crosshairs include Seven Group Holdings (ASX:SVW), REA Group (ASX:REA), Lovisa (ASX:LOV) and Audinate (ASX:AD8). At current prices we aren’t confident that these investments will outperform the market over a longer timeframe (given lofty expectations) but if we feel this shift to our favour – we won’t hesitate to pull the trigger.

In the meantime, we see value for members at current levels in some of our Star Stocks. Three companies I would point out are:

Interested In Learning More About Stock Doctor’s Market Edge?

The power of Stock Doctor’s Financial Heath model and investment methodology is twofold. Not only do we help investors discover superior Growth stocks – but we also play an integral part in avoiding the losers.

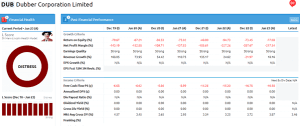

Avoiding the businesses with unsustainable balance sheet, mounting losses and speculative revenue models. A perfect example of this is how we avoided the disastrous announcement by Dubber Corporation, which remains in voluntary suspension due to fraudulent activity in the company’s cash holdings. We have been flagging risks in the business for years – particularly highlighting how revenue grew at elevated levels, but cash flow losses continued to mount.

To discuss the future of your investments in detail, book in a free consultation with a Lincoln representative.

To discuss the future of your investments in detail, book in a free consultation with a Lincoln financial expert.