In the realm of investing, passive strategies have surged in popularity, driven by their promise of simplicity and cost-efficiency. Originating in the mid-1960s, passive investing has become a cornerstone of the retail investment landscape, sparking lively debate on its broader market implications. As we delve deeper into this phenomenon, it is crucial to explore both the merits and potential pitfalls of passive investment products, including concerns that extreme adoption could result in distorted price discovery and eventual misallocation of capital.

“If you push indexation to its logical extreme, you will get preposterous results” – Charlie Munger

The Birth of Passive Investing

Passive investing is not really an investment strategy per se, but rather an endorsement of the efficient market hypothesis (EMH), a theory that was introduced by the University of Chicago professor Eugune Fama in the 1960s. The central idea behind EMH is that it is impossible to consistently achieve higher-than-average returns by analysing and trading on publicly available information because prices already incorporate that information. Assuming these conditions are true, a rational investor should seek the “market” return at the lowest possible cost by buying all stocks in the investable universe and positioning them according to their prevailing market valuations.

The genesis of passive investing products can be traced to Jack Bogle, the founder of The Vanguard Group. Mr Bogle was a significant proponent of index investing, having introduced the first retail index product, the Vanguard 500 Index Fund, which aimed to replicate the performance of the S&P 500. Today, Vanguard is the largest fund manager in the world, alongside BlackRock, managing some $8 trillion USD. Putting some context to that number…..that is approximately 3 times greater than the entire market capitalisation of the Australian stockmarket!

Understanding how the products work

The raw mechanics of passive investment involve constructing a portfolio that mirrors an index’s holdings in proportion to their market capitalisation. For example, in an ASX 300 index fund, the fund manager aims to hold shares of each of the 300 companies in the same weight as represented in the index. This approach ensures that the fund’s performance closely mirrors that of the underlying index.

To sustain this alignment, passive funds undergo periodic rebalancing. This involves adjusting holdings in response to changes in the index’s composition due to corporate actions like stock splits, mergers, or shifts in market capitalisation. This process ensures that the fund continues to accurately represent the market segment it tracks.

Investors can usually buy and sell shares of passive investment products on stock exchanges, much like individual stocks. Exchange Traded Funds (ETFs) offer intraday trading flexibility, allowing investors to execute trades throughout the trading day at market prices.

When investors buy shares of an ETF, they are buying them on the secondary market from other investors or market makers, not directly from the fund itself. However, when significant demand for the ETF outweighs sellers in the secondary market, authorised participants (typically large institutional investors or market makers) can create new shares of the ETF. The Authorized Participant takes delivery of new securities from the issuer in exchange for either cash, or a portfolio of securities that mirror the composition of the ETF’s benchmark index. Either way, the end result is an increase in the size of the fund in the same proportion as the index, regardless of price. The whole process is very efficient. However, as we saw from the global pandemic, efficiency can expedite change in either direction, both good and bad.

Exploring the growth

The structure of the investment management industry has evolved rapidly. Proponents of the change will reasonably argue that investors have benefited from more competitive costs, whilst industry innovation has allowed for easier access to all investments via exchange traded funds, online verification forms, etc.

But the rise to dominance of passive investment managers has been at the crux of the structural change. If you do not believe me, just look up the share registry of any large company in the world. 9 times out of 10, the names of Vanguard or Blackrock will feature prominently on the top of the list.

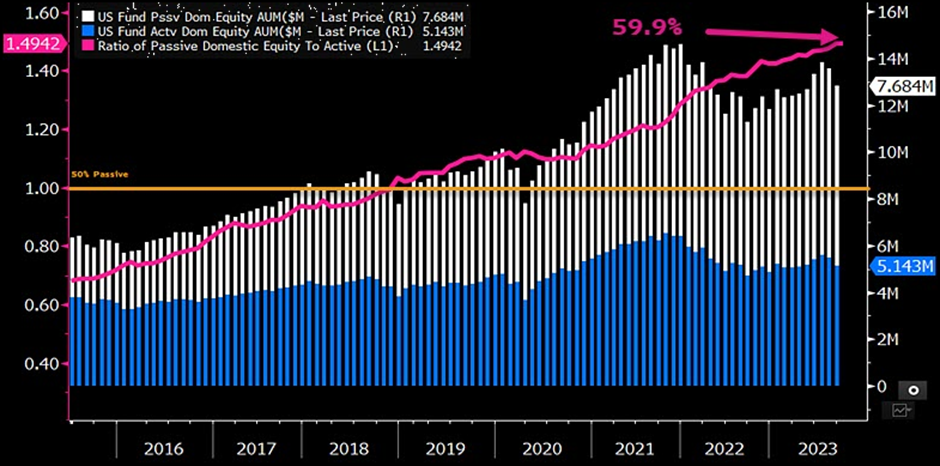

In the US, the birthplace of passive, the numbers are startling. The below chart illustrates the market share of assets under management between active and passive. Passive has recently overtaken active and there is no apparent end in sight. In fact, the pace of market share growth is accelerating.

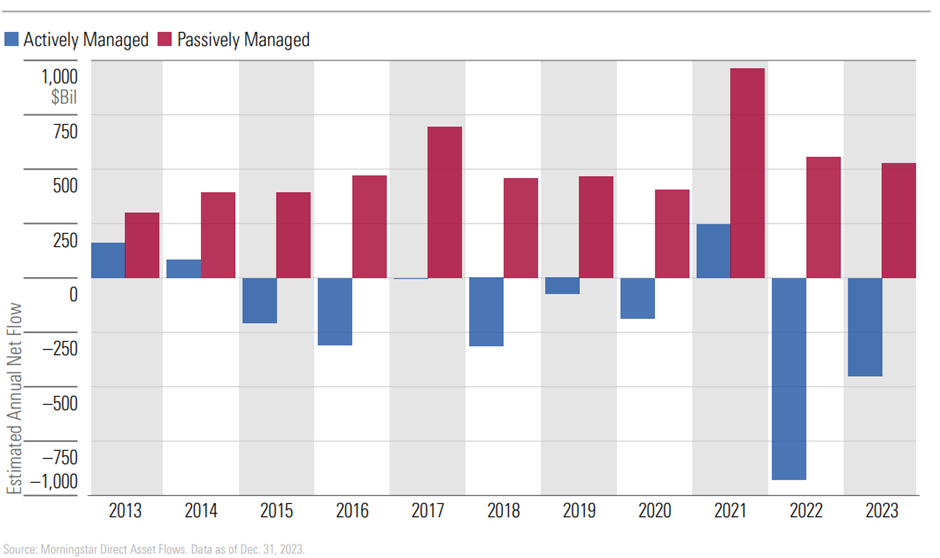

The flows from Morningstar data reflect this dynamic. Active strategies have only had positive net flows into their funds 3 times in a decade. Each time that happened, it was dwarfed by positive passive flow.

Why are passive products dominating investment flows?

The reason for this is simple; they offer very low fees, efficient access, and “better” historical performance outcomes.

The gatekeepers to the bulk of investment flows include financial advisors and asset consultants. These days, you would be hard-pressed to find any advisor or consultant who does not endorse a passive investment approach for their clients. Why try to out-think and out-smart their competitors when the “market return” is most often better than the alternative? And the benefit to them for this mentality is that they can also save on costs because they need not do any real due diligence about which active manager offers the best investment product – just “buy the market return” and avoid the headaches of having to articulate why the active manager “underperformed” the index.

This very mentality will drive increasing flows into passive products, further perpetuating market vulnerabilities.

Why should we be alarmed?

Passive investing and its utility is based on a fundamental assumption. It requires active participants in the market to remain the linchpins of price discovery. The whole thesis of efficient markets breaks down if a significant influence on the volume of market transactions is totally indifferent to information. Passive investment vehicles act on flow, and flow alone. If you put money into a passive strategy, it goes straight into the market. Investors in these funds will buy the good, bad and the ugly companies in proportions that an already disrupted marketplace has determined to be the fair price. There is no consideration given to valuation, fundamentals, liquidity….. none of it.

All works well if active managers, the real servants of price discovery, continue to have a controlling influence on the market. But as described previously, the balance has already shifted.

Sometimes, the architects are best positioned to articulate their own design flaws…

“If everybody indexed, the only word you could use is chaos, catastrophe…the markets would fail.” Jack Bogle

Readers who wish to gain a deep understanding on this topic, I recommend they follow the work of Michael Green, a prominent investment manager in the US who has tirelessly shone a light on the evolving systemic risks and the worrying influence that passive investing behemoths have on the regulatory environment.

Summary

Passive vehicles are indifferent to investment fundamentals because they are replicating indices that were not designed as investment strategies. Instead, they were created for observational purposes. The team at Standard & Poor’s were not attempting to sell brilliant investment advice when they launched the S&P500 index. It was intended to be used as a scorecard for active investment managers to assess the performance of their own strategies.

But here we are! Most portfolios are being designed around an index construction methodology that was never intended to be taken as investment advice. When capital allocation continues to flow into vehicles that do not consider investment fundamentals, we end up with a dysfunctional market that allocates capital inefficiently and is vulnerable to major volatility. We have already entered this paradigm, with observations including:

Extreme concentration risk of indices. The “Magnificent 7” make up ~30% of the entire S&P500 Index.

Corporate boards making corporate actions influenced on index inclusivity. “If we acquire company Z, then we will be included in the S&P500.”

Increasing stock correlation. If flow is all that matters to share prices, stocks will tend to behave increasingly similar.

Many of these topics will be explored in greater detail over the year, but I would encourage members to consider the risks after being advised to “buy the market”.

The importance of conducting due diligence cannot be underestimated. As outlined throughout the article, these products lack the dynamic management that traditional active products conduct via a team of investment professionals. By design, passive strategies are in effect, on autopilot. Hence, investors must be ready to take control during market turbulence. This is where Stock Doctor can provide guidance.

Nevertheless, utilised judiciously and managed effectively, passive investment funds can enhance portfolios through diversification, risk management, and thematic exposure. But it should never be the predominant position in a well-managed investment portfolio given the apparent design flaws.

There is much more to unpack, but this is a good start to a longer conversation.

All financial services are provided by Lincoln Indicators Pty Ltd ABN 23 006 715 573 (Lincoln) as the Corporate Authorised Representative of Lincoln Financial Group Pty Ltd ABN 70 609 751 966, AFSL 483167.

Book a Chat

To discuss the future of your investments in detail, book in a free consultation with a Lincoln representative.

Register your interest

To discuss the future of your investments in detail, book in a free consultation with a Lincoln financial expert.

Stay updated with the latest on the numbers.

Receive regular market tips and insights to your inbox.

Sign up to unlock this exclusive content.

All new sign-ups receive our investor whitepaper and information about upcoming news and events.