The current ASX reporting season is in sharp focus as businesses reveal how they fared in the latter half of 2020, an eventful period punctuated by lockdowns and government stimulus.

So far, earnings have generally come in better than expected and since releasing results, more than 60% of stocks are outperforming the market. Of these, it’s largely cyclical growth businesses that are outperforming, including the banks and insurers, fund managers, building materials, and retailers. A fact that highlights the importance of investors having adequate exposure to high-quality cyclical growth stocks in their portfolios during this post-recession economic recovery.

Today we reveal five Stock Doctor Star Stocks that have delivered impressive results this reporting season.

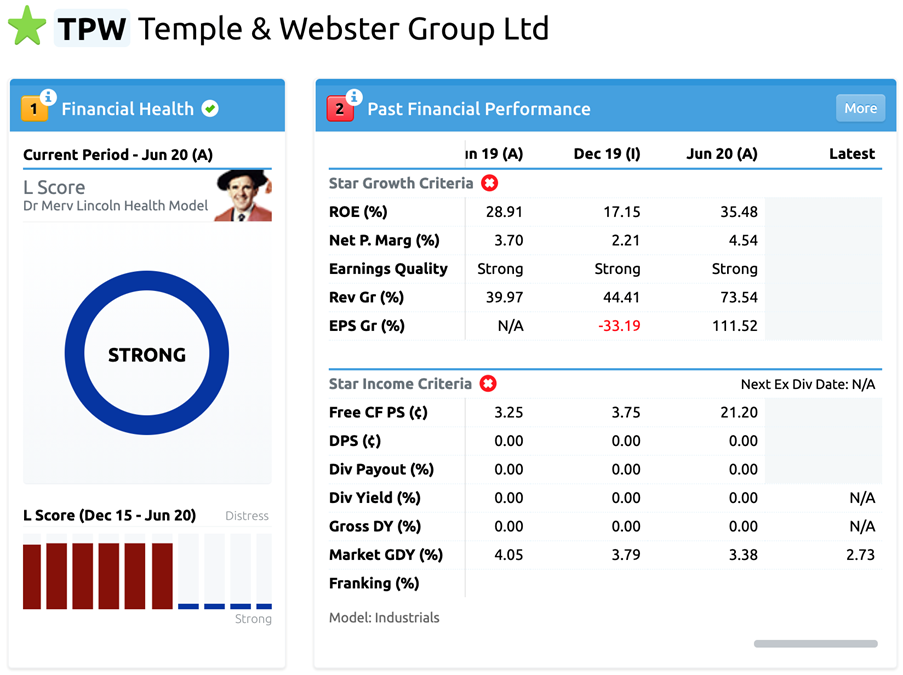

Backed by government stimulus and a pick-up in consumer spending, many retailers have reported strong profits. A standout in this sector has been Temple & Webster (TPW).

Operating in the online homewares and furniture space, TPW, delivered strong results for the first half of FY21 as people spent a significant amount of time at home amid lockdowns and travel restrictions.

As a pure online retailer, the company is not saddled with the high rental costs of brick-and-mortar stores and by keeping costs low, TPW can generate a high return on equity. It has also benefited from increased brand awareness following COVID.

For the half year period ending 31 December, the company reported strong organic growth numbers, which we expect to continue. Total sales revenue increased 118% over 1H20 to $176.3M as TPW capitalised on consumers shifting their discretionary spend into their homes.

The company continues to invest, having released a mobile app, and is expanding its product offering and launching retail showrooms. It has also delivered its first national marketing campaign to improve brand awareness.

Confident that earnings growth will continue even as people return to the office, we have added TPW to our Borderline Star Growth Stock universe.

Also impressive in the retail sector has been Breville Group Limited (BRG), a developer and distributor of premium small electrical kitchenware with a prominent retail brand and a presence in both domestic and global markets.

As individuals shifted to work from home and redirected spending away from holidays and social events, the first half of FY21 saw the company record impressive results.

During the half year, the company boasted healthy net profit margins, lifted its earnings efficiency, and had a significant improvement in operating cash flows. It has maintained a strong position of Financial Health with minimal debt and a net cash position of ~$90 million.

As well as the work from home thematic, the company’s solid first half result was underpinned by its continued expansion across global geographies, including its core European and North American markets. Its European operations were seemingly unimpacted by COVID, and its inventory build-up in prior periods helped buffer the supply chain limitations from BREXIT.

As a result of its strong performance and positive outlook, we have upgraded BRG from Borderline to Star Growth Stock status. BRG is a quality business and management’s ability to grow market share, particularly in America and Europe, is a testament to its ability to identify and drive shareholders’ value.

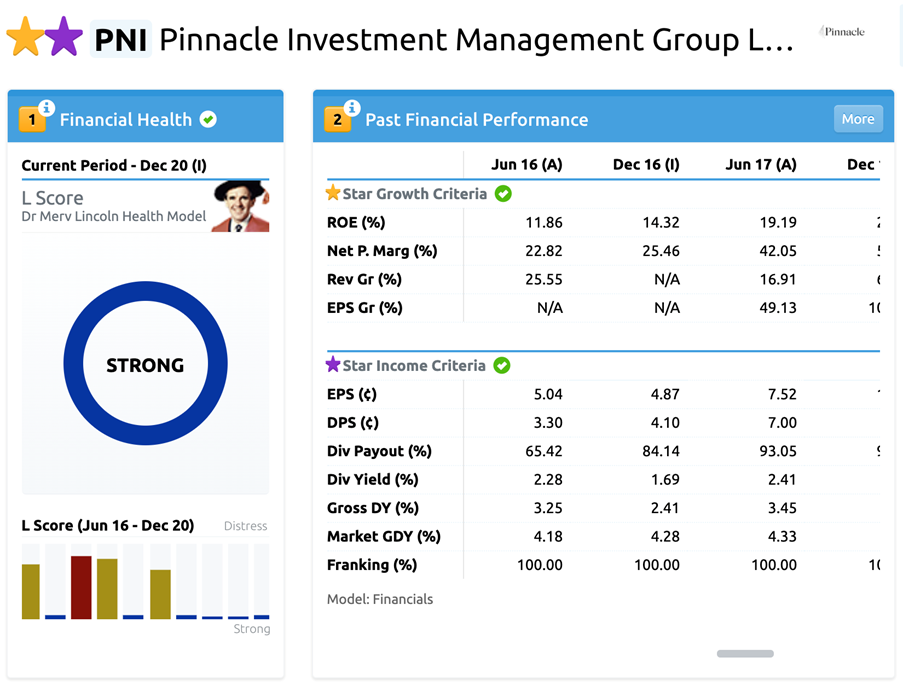

Pinnacle Investments (PNI) — an investment group that holds ownership stakes in several emerging and promising fund managers (also known as affiliates) — exceeded consensus expectations in 1H21, a result that saw us upgrade the company to Star Growth and Star Income Stock status.

Led by strong performance in equity markets, revenue grew by ~28% in 1H21, lifting net profit after tax by ~120% to $30.3M, well above consensus estimates of $22.1M.

A substantial outperformance in fees saw profit margins surge to 64% (vs 56% 1H20), driving an expansion in return on equity from 20% in 1H20 to 25%. Half year annualised earnings per share (EPS) was up 40% from a year earlier.

PNI will pay an 11.7 cent per share interim dividend, representing a 70% payout ratio on EPS — a sustainable level.

We expect earnings growth to remain strong for the rest of the year, as total revenue has historically been skewed towards the second half when affiliates performance fees tend to be received. Supporting this view is a positive outlook on financial markets, affiliate fund managers continuing to outperform benchmarks, and a higher mix of funds under management (FUM) exposed to performance fees.

Management didn’t provide guidance but did allude to the ongoing potential to deliver significant performance fees in 2H21. The full year consensus forecast points to EPS growth of ~74%.

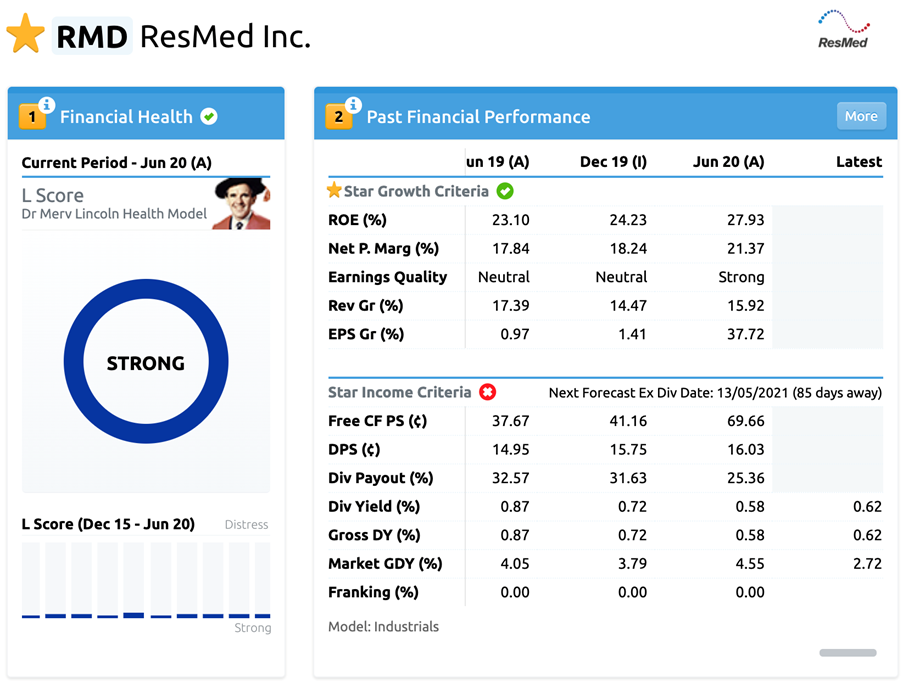

Star Growth Stock, Resmed Inc (RMD) — a company that develops breathing devices and sleeping devices — delivered a solid result for the quarter ending 31 December.

Performance was driven by an improvement in new patient volumes and uptake of mask/accessories within its core sleep apnoea segment, and higher adoption of digital health and out-of-hospital healthcare programs.

During the period, the company saw continued solid mask and accessories growth driven by resupply purchases by patients. Sales outside of the US were particularly strong, suggesting a recovery in key markets such as Europe and Asia which were each up 17% on the prior year. An obvious risk is a slowdown in ventilator sales, but RMD only has a 5% revenue exposure to ventilator demand.

Going forward, the company’s competitive advantage is supported by its healthy margins, new product launches, and high R&D spend. We believe RMD is well-positioned to achieve growth in FY21, based on the continued strong operating momentum.

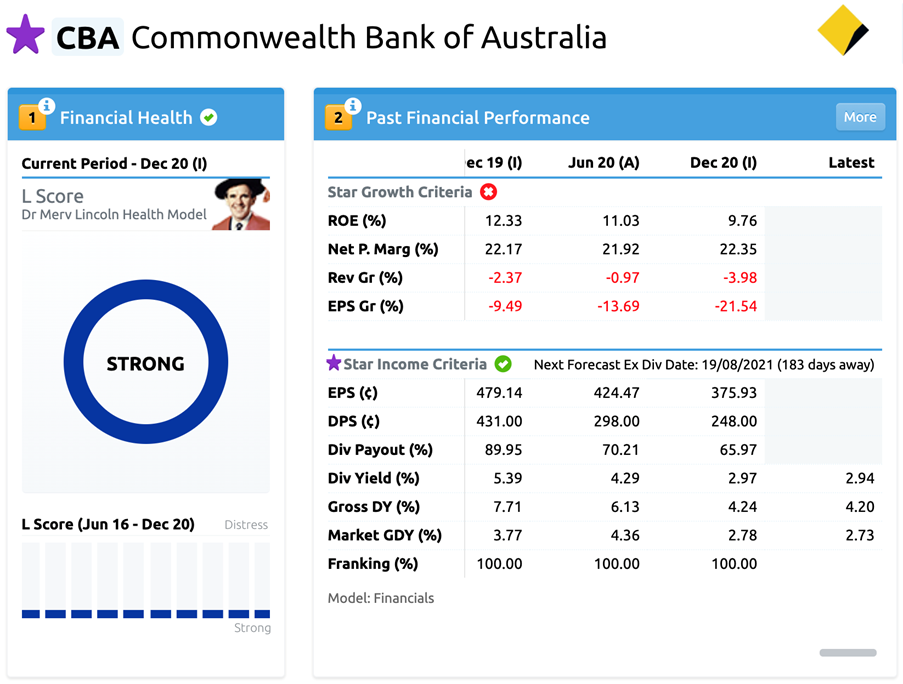

Often considered a bellwether for the Australian economy, leading Australian bank and Star Income Stock, Commonwealth Bank (CBA) reported a better-than-expected earnings result for 1H21.

Already in a strong capital position, the quicker than expected economic recovery benefited CBA with strong growth in residential housing and business lending. And with more people able to service their loans, bad debt charges decreased in the latter half of 2020. The bank’s divestment of Colonial First State and CommInsure Life also freed up some funds.

The bank increased its first half dividend to $1.50 per share, up from 98 cents in the prior half year, implying a cash earnings payout ratio at a sustainable 67% — below CBA’s target of 70-80%, suggesting dividends could rise in 2H21. At the current price, the forward grossed-up yield is approximately 4.2%.

Perhaps unsurprisingly, travel and leisure are not looking healthy, while reports from the energy sector have also been underwhelming. Companies that primarily derived income offshore have also been hampered by strength in the Australian dollar.

Fortunately, poor results typically don’t come from nowhere and with Stock Doctor’s Financial Health model, we had the heads up on which businesses were facing hardship.

Our Financial Health model has helped members avoid some of the biggest underperformers so far in this reporting season, including Cimic Group Limited (CIM), Challenger Limited (CGF), and Worley Limited (WOR).

Despite their Marginal (CIM, WOR) and Distressed (CGF) Financial Health scores on Stock Doctor, each rallied strongly prior to releasing results, only to fall back sharply, demonstrating the importance of paying attention to the financial health of a business even if its poor quality was not reflected in its share price.

Financial Health should form the foundation for all investment decisions as without understanding the true financial quality of a stock, you are purely speculating and risking serious loss.

For over 30 years, our Financial Health methodology and renowned Star Stock recommendations have helped our members and investors make confident and informed decisions, in all market conditions.

Stock Doctor separates quality businesses from potential disasters and we invite you to trial Stock Doctor for free. You’ll receive access to every one of our Star Stocks, selected for income focused and growth investors.

The information in this communication is market commentary only and reflects Lincoln’s views and beliefs at the time of preparation, which are subject to change without notice. To obtain up-to-date information, please contact us.

To discuss the future of your investments in detail, book in a free consultation with a Lincoln representative.

To discuss the future of your investments in detail, book in a free consultation with a Lincoln financial expert.